Introduction

Mortgage interest rates play a vital role in the housing market, influencing home affordability and buyer confidence. As of late 2023, understanding the factors driving these rates is essential for potential homebuyers, policymakers, and economic analysts alike.

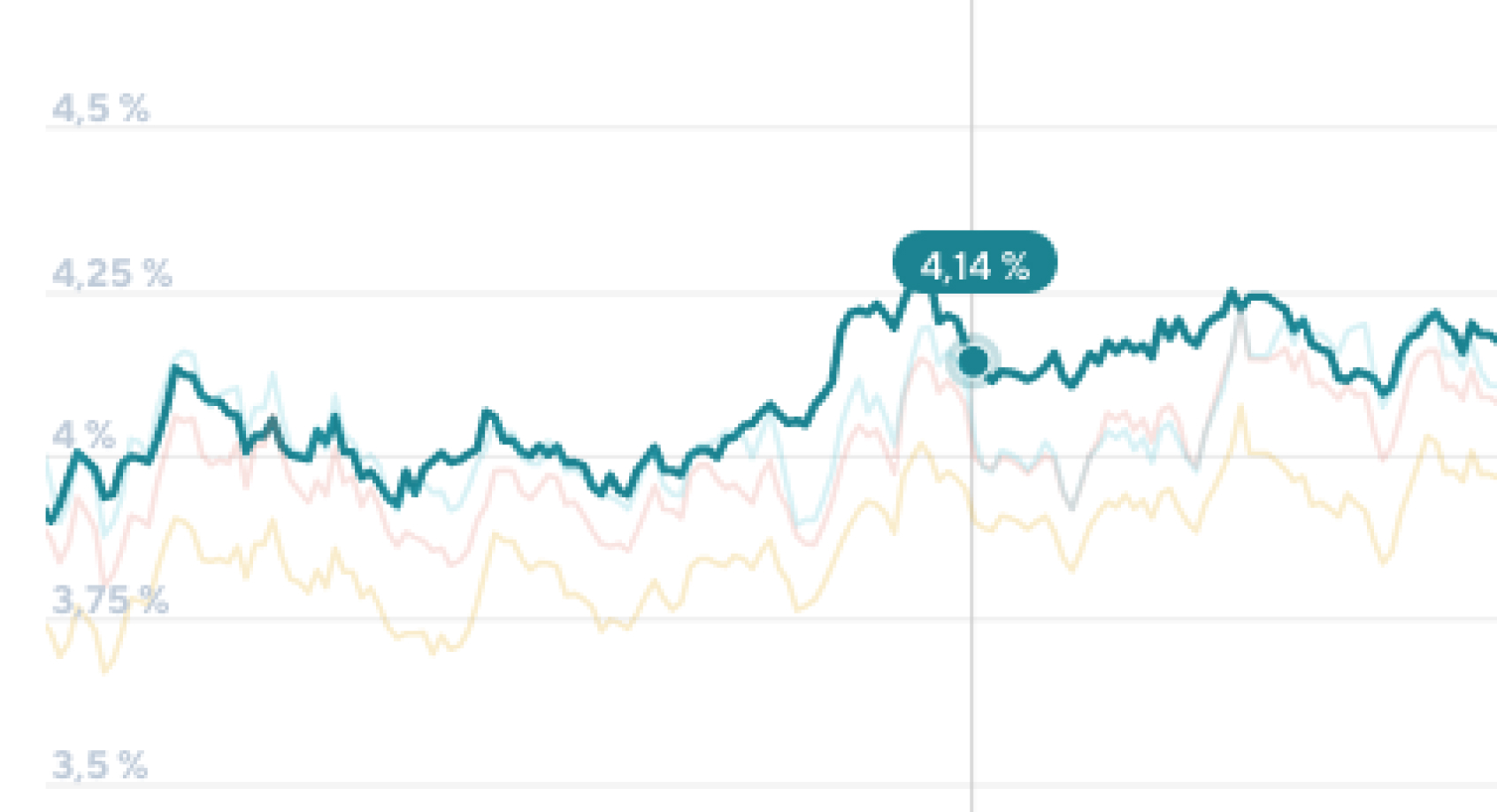

Current Trends in Mortgage Interest Rates

As of October 2023, the average mortgage interest rate for a 30-year fixed mortgage hovers around 7.5%, a noticeable increase from the historic lows experienced in 2020 and 2021. This rise is primarily attributed to the Federal Reserve’s aggressive interest rate hikes aimed at combating inflation, which has remained persistently high.

Experts indicate that the Fed’s recent decisions to increase benchmark rates by 0.25% several times over the past year have had a cascading effect on mortgage rates. Such increases affect lenders’ costs and, consequently, the rates that consumers face when securing loans. Additionally, economic uncertainty and fluctuations in the housing market contribute to the general volatility of mortgage rates.

Factors Influencing Mortgage Interest Rates

Several key factors influence mortgage interest rates, including inflation, employment rates, and economic growth. With inflation currently around 3-4%, the Fed continues to prioritize stabilizing prices, which could signal further rate increases in the near future. Should inflation rates decrease significantly, analysts predict a potential stabilization or even reduction in mortgage rates, encouraging home buying.

Moreover, unemployment rates are at record lows, allowing for increased consumer confidence. However, should economic conditions shift abruptly, this could also impact future mortgage rate trends. Housing inventory remains low, which pressures prices upward, further complicating buyers’ decisions.

What This Means for Homebuyers

As mortgage interest rates remain elevated, prospective homebuyers must adjust their expectations and strategies. Increased rates translate to higher monthly payments and, subsequently, lower loan amounts that buyers may qualify for. Many buyers are now opting for adjustable-rate mortgages (ARMs), which offer initially lower interest rates but can fluctuate over time, making budgeting more challenging.

Conclusion

In conclusion, mortgage interest rates are influenced by a complex interplay of economic factors that homeowners and buyers need to navigate. As rates remain high, it is vital for potential buyers to stay informed and consider waiting for more favorable terms or exploring alternative financing options. Looking ahead, any signs of economic stabilization may present opportunities for those looking to buy homes in the coming months. Staying abreast of economic developments is crucial for making informed mortgage decisions.