Introduction

FICO scores play a vital role in personal finance, as they are a key factor in determining an individual’s creditworthiness. These three-digit numbers, developed by the Fair Isaac Corporation, influence financial decisions made by lenders, landlords, and insurance companies. Understanding FICO scores is essential for individuals aiming to secure loans, credit cards, or rental agreements, making it an increasingly relevant topic in today’s economy.

What are FICO Scores?

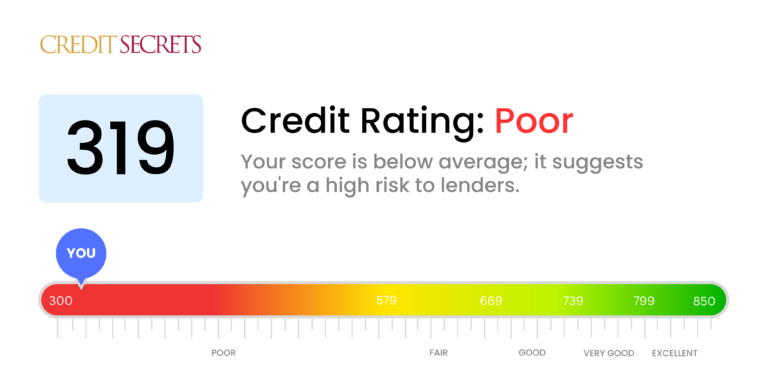

FICO scores range from 300 to 850, with higher scores indicating better creditworthiness. The score is calculated based on five key factors: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and types of credit used (10%). The importance of maintaining a healthy FICO score cannot be overstated, as even a slight increase can significantly lower interest rates on loans and credit cards.

Recent Trends and Events

As of October 2023, FICO scores have seen an average increase across the United States. In light of changing economic conditions, including rising interest rates and inflation concerns, consumers have shown an increased awareness of their credit scores. Recent data from FICO indicates that about 30% of consumers are now checking their scores at least monthly, a significant rise compared to previous years. This trend correlates with a surge in educational resources available through financial institutions and credit monitoring services, helping individuals better understand and manage their credit.

The Impact of FICO Scores on Financial Decisions

FICO scores directly impact a range of financial decisions. Lenders use these scores to determine loan eligibility and interest rates. For example, a person with a FICO score of 720 may qualify for a top-tier mortgage rate, while someone with a score of 620 may only qualify for subprime lending, resulting in higher payments. Additionally, landlords often assess FICO scores when renting properties. A poor score could lead to higher security deposits or even denial of rental applications.

Conclusion

In conclusion, understanding FICO scores is crucial for anyone seeking financial stability. With the increasing trend of consumers monitoring their credit scores, it is imperative to maintain a good score through responsible credit practices. As economic conditions fluctuate, keeping an eye on one’s FICO score can lead to better financial opportunities. Moving forward, consumers should prioritize understanding what affects their scores and take proactive steps to improve them, ensuring they are prepared for necessary financial decisions.