Introduction

VA loans are a beneficial financial product designed to assist veterans and active-duty military members in obtaining home financing. With a unique structure that eliminates the need for a down payment and offers favorable loan terms, these loans play a critical role in supporting those who have served the nation. Understanding VA loans is important as they provide a pathway to homeownership for many who may struggle with the conventional lending process.

What are VA Loans?

VA loans are mortgage loans backed by the United States Department of Veterans Affairs (VA). Initiated in 1944 as part of the G.I. Bill, VA loans are specifically tailored for veterans, active duty service members, and certain members of the National Guard and Reserves. The fundamental benefit of VA loans is the zero down payment requirement and competitive interest rates, which makes homeownership more accessible.

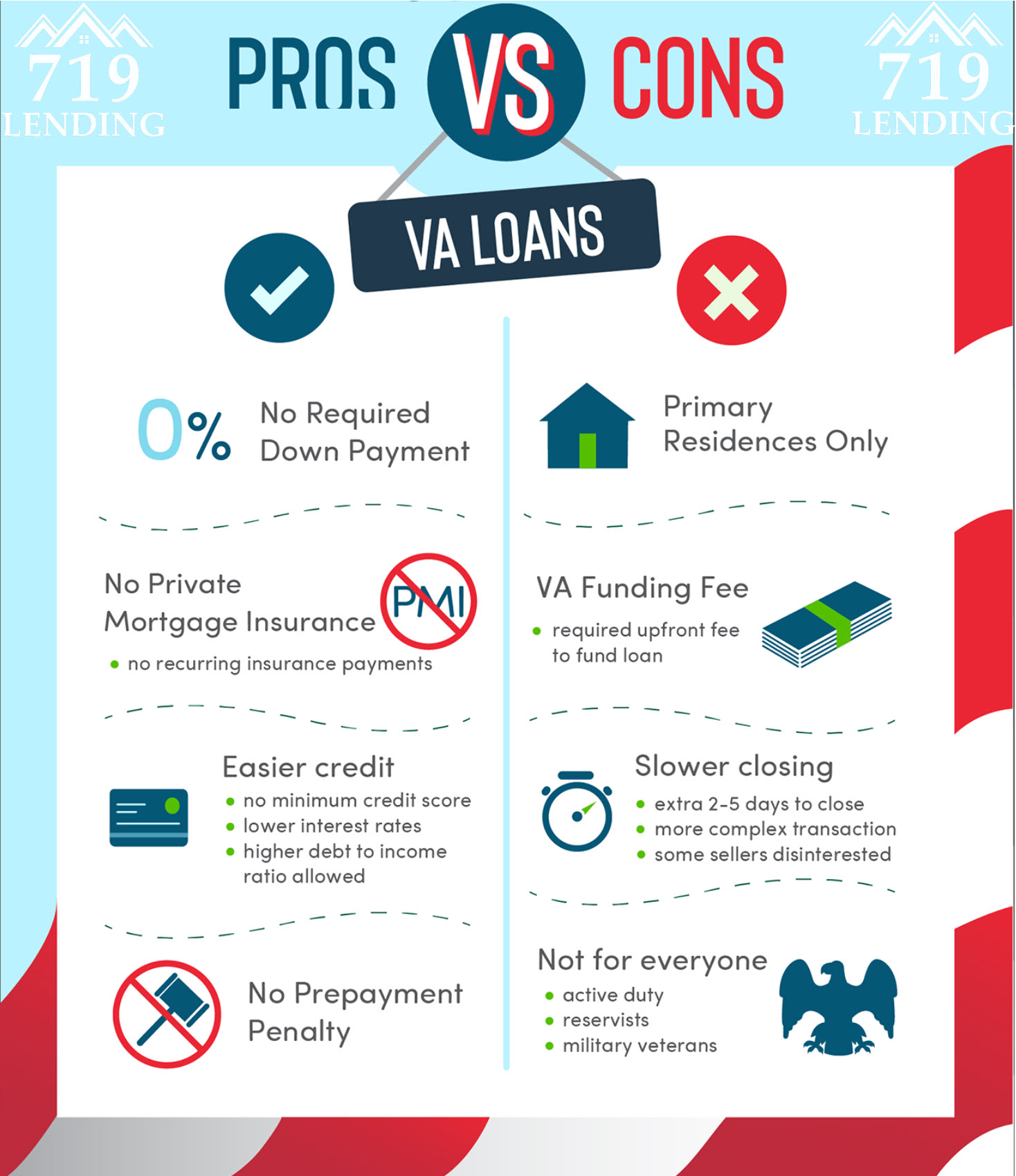

Key Benefits of VA Loans

- No Down Payment: Many lenders allow qualified borrowers to purchase a home with no down payment, which significantly lowers the initial cost of buying a home.

- No Mortgage Insurance Premium: While conventional loans typically require private mortgage insurance (PMI) when the down payment is less than 20%, VA loans do not require PMI, resulting in considerable savings.

- Competitive Interest Rates: VA loans often feature lower interest rates than conventional loans, which can lead to substantial savings over the life of the loan.

- Flexible Credit Requirements: VA loans tend to be more forgiving concerning credit scores, providing opportunities for borrowers who might not otherwise qualify for a mortgage.

Eligibility Requirements

To qualify for a VA loan, applicants must meet specific service requirements. Generally, you must have served in the active military, naval, or air service and been honorably discharged. Additional eligibility criteria include:

- Current service members with at least 90 days of consecutive service during wartime or 181 days during peacetime.

- Veterans who have served a minimum period of time and were discharged under conditions other than dishonorable.

- Surviving spouses of service members who died in the line of duty or due to a service-related disability may also be eligible.

Conclusion

VA loans provide a vital resource for veterans and active-duty personnel seeking homeownership without the financial burden of a large down payment or insurance costs. As the demand for housing persists, understanding the potential benefits and requirements of VA loans is crucial for eligible borrowers. With the housing market showing a potential upturn in the coming months, prospective homebuyers should consider leveraging their eligibility for VA loans to secure homes. The VA loan program stands as a testament to the country’s commitment to support its military service members, making homeownership more achievable for those who have sacrificed for their country.